A Legal Analysis of Spain’s Social Security for the Self-Employed (RETA)

Under current Spanish law, all workers, whether employees or individuals engaged in independent commercial activities, must be enrolled in the national social security system. For the latter, commonly known as freelancers or self-employed individuals (‘autónomo’ or ‘trabajador por cuenta propia’ in Spanish), the specific social security scheme is the ‘Special Regime for Self-Employed Workers’ (Régimen Especial de Trabajadores Autónomos), or RETA. This is often colloquially referred to as ‘boss insurance’ within the Chinese community.

RETA: Mandatory Obligation and Scope

Contributing to RETA is a mandatory legal obligation for the self-employed. Any individual who regularly carries out a commercial activity, whether as a natural person or through a corporate entity, must register and pay contributions on time. The law’s definition of ‘commercial activity’ is very broad, covering all sectors such as services, manufacturing, and retail, and it does not distinguish between online activities (like online tutoring or e-commerce) and operating a physical store. The core objective of this system is to provide workers with basic social protections, including benefits for unemployment, sickness, and work-related injuries.

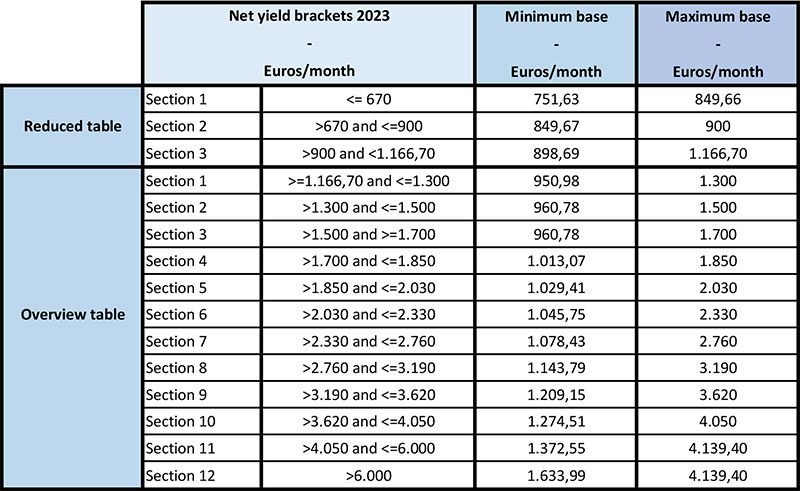

Monthly Contributions: Standard Rates and Startup Incentives

RETA contributions are paid monthly. The standard amount is not fixed but is calculated dynamically based on the self-employed individual’s annual net income, typically around €300 per month. However, to encourage entrepreneurship, the Spanish government offers a significant reduction for those registering for the first time. During the first year of business, new entrepreneurs only need to pay a reduced flat rate of around €90 per month, which greatly lowers initial operating costs.

Dual Registration: Social Security and Taxes

To become a legal self-employed worker, in addition to registering for RETA with the Social Security authorities, one must also complete the corresponding tax registration with the Spanish Tax Agency (Agencia Tributaria). After completing tax registration, the self-employed are required to file quarterly income returns. It is worth noting that tax registration itself does not automatically mean you have to pay taxes. The tax due is calculated based on net profit (i.e., total income minus all deductible business expenses). If there is no income in a quarter, or if deductible expenses exceed income resulting in a loss, no income tax is payable.

Social Security Responsibilities for Company Directors

A common misconception is that forming a company (such as a limited liability company, S.L.) exempts an individual from the obligation to pay ‘autónomo’ social security. This is not the case. The law stipulates that as long as an individual actively works, provides labor, or performs management functions within the company, regardless of whether they are a shareholder, they must register as an ‘autónomo’ and pay the corresponding contributions. The only exception is for purely passive investors—that is, individuals who only contribute capital to become shareholders but are not involved in any of the company’s actual operations or management. They are not required to contribute to RETA.